EMoney

EMoney Fidelity

Fidelity Schwab

Schwab

Roth Conversions and Tax Rate Arbitrage: Not As Confusing As It Sounds

When Your Income Dips, Convert to Roth

Arbitrage is a fancy word used in finance conversations by people that really want to seem smart.

Today, I’m excited to be one of those people.

Roth conversions during low-income years can be a great way to set money free forever at a reduced tax rate. This strategy works well for those that have accumulated a high balance in traditional IRA or 401(k) through pre-tax contributions, and will have a low-income year because they’re quitting their jobs to:

1. Retire

2. Start a business

3. Stay home with the kids

4. Find themselves on yoga retreat, become a social media influencer, and sell leggings on Facebook (come on, we all know them)

But first…

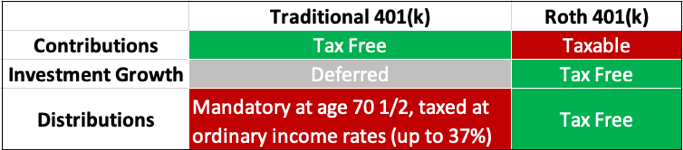

Roth Accounts: Why Are They So Attractive?

The difference between Roth and traditional retirement accounts is like the difference between an all-inclusive resort vs. a hotel.

Suppose you’re planning a dream vacation after a long year of work, kids, etc. Hotels seem reasonable, but seven days of eating and drinking at bars and restaurants looks VERY expensive. Then you see an advertisement for an all-inclusive resort where you’ll stay in similar accommodations and have access to similar bars and restaurants. For your desired week, the all-inclusive package is slightly more money.

Is it worth paying a little more now, knowing that you can eat and drink until someone has to carry you off the beach like a sea mammal? What’s the value of the endless open bar and buffet?

Roth accounts are like open bars and all you can eat buffets. You pay tax ONCE and can pile on filet mignons and rock shrimp at no additional cost.

One would have to agree that, if price and quality of the all-inclusive vacation is the same or better than the “do-it-yourself” strategy, then all-inclusive is the better choice.

Assume our vacationer looked at the all-inclusive packages for different weeks and found that the price for the following week was 25% cheaper. Where it was a close call before, now it’s a no-brainer. Go all-inclusive.

Roth accounts are all-inclusive. Investors pay tax once on Roth contribution funds, but never again—the funds are free forever.

Traditional accounts allow “free entry” with all sorts of taxes and rules afterwards.

This is why, all else being equal, Roth is better than traditional. But what if the all else is NOT equal?

What can change?

Answer: Tax rates.

The Concept of Arbitrage

Arbitrage is buying something for $1 solely to immediately sell it for $2. If you see an ad that says, “Tom Brady-Signed Football Wanted: Will Pay $300”and then you see a Tom Brady- signed football for sale for $150—you might buy the ball, sell it, and make $150.

Congratulations, you can now tell people that you’re an “arbitrager” at cocktail parties.

The “price” of contribution to Roth vs. Traditional is your tax rate in a given year. The value is based on your anticipated tax rates in future years, or alternatively, the tax benefit of deferral in prior years.

Planning to fund Roth IRAs is all about tax rate arbitrage. High earners have high tax rates, and generally contribute to 401(k)s pre-tax because the savings is so attractive (upwards of 45% for every contributed dollar).

If for some reason income drops (retirement, time off, starting a business), tax rates drop as well. Now, folks can convert their traditional IRAs to Roth IRAs at a much lower tax rate.

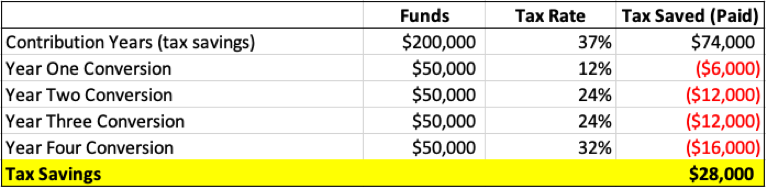

Here’s an example: Mandy is a high-earning employee with a combined tax rate of 45%. After five years of maxing out her 401(k), she plans to leave her job and start a consulting business. While she has plenty of savings to cover expenses (due to working with a great financial planner), she’ll have very low income in Year 6—her new tax bracket is 12%, and gradually goes up as her business grows.

She should take a portion of her savings and convert it to a Roth IRA. Here’s a visual:

This is how it works: during her working years she made $200,000 of pretax contributions, which at a 37% rate saved her about $74,000 in taxes (this is temporary savings). In converting to Roth in low income years she saved the “spread” between tax rates.

“Spread” is a term often used in arbitrage conversations—make sure to say it, constantly.

It just means the difference in tax rates and dollars saved. $50,000 taxed at 37% vs. 12% creates a tax rate spread of 25%, and a dollar spread of $12,500. This is cover charge savings. It has cost $12,500 less to set $50,000 free forever.

The key to this strategy is understanding your tax situation, and how your rates might change in the coming years.

This is not rocket science, it's just "getting a good deal" on Roth account funding.

A financial plan that looks out at least five years is helpful here.

Also, be careful that Roth conversion income doesn’t bump you into a new tax bracket. Tax projections are very helpful here. That's why you should work with a planner....

Disclosure: Claro Advisors LLC ("Claro") is a registered investment advisor. Advisory services are only offered to clients or prospective clients where Claro and it's representatives are properly licensed or exempt from licensure.

Past performance shown is not indicative of future results, which could differ substantially.

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor's particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor.

The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward‐looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

Index returns are unmanaged and do not reflect the deduction of any fees or expenses. Index returns reflect all items of income, gain and loss and the reinvestment of dividends and other income. You cannot invest directly in an Index.