EMoney

EMoney Fidelity

Fidelity Schwab

Schwab

The TRUE Value of Financial Advisors

Work With Someone That Does It All

In a prior article I explained how advisors add value to investment accounts, but the value of financial advice extends well beyond investments. Worthwhile financial advice professionals should seek to grow and protect a client’s total net worth—rather than simply maximize investment return on liquid assets.

This is why folks should work with a financial planner.

In order to increase a client’s total net worth, the planner needs to do two things:

1. Encourage consistent saving

2. Encourage consistent investment

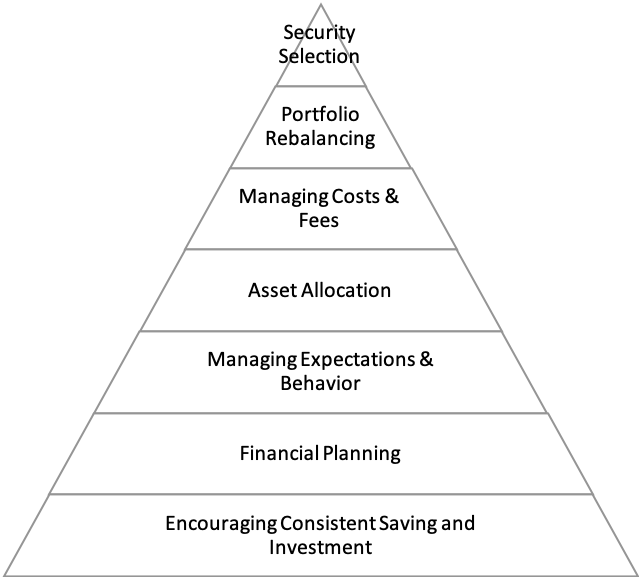

THE HIERARCHY OF ADVISOR VALUE

Consistent savings and investment over several decades will make a meaningful difference in a client’s financial position. Strangely enough, these two things have been shown to be the true value of a financial advice professional.

The problem for most financial advisors is that they don’t know how to do this. Why? Because they aren’t trained to do anything other than “run money”, which is an outdated industry term for putting clients into investment models or picking stocks.

Encouraging consistent saving and investment requires an advisor to provide (1) expertise, (2) effort, and (3) accountability. Let’s take them one by one.

Expertise

This would include enough knowledge “to be dangerous” in the following areas, with an expertise in one or more:

1. Income taxes

2. Equity compensation

3. Employee benefits

4. Balance sheet analysis

5. Social Security, pensions and Medicare

6. Charitable giving

7. Education planning

8. Retirement withdrawal planning

9. Estate planning

10. Insurance

11. Small business ownership and transition

While many advisors claim to have this knowledge in these areas, they really only offer advice when it can create a revenue generating activities through commissionable transactions or manageable assets.

Here’s an example. Most advisors claim to know about “business planning”. I would imagine business planning to involve consistent analysis and advice on core business financials and metrics in an effort to grow enterprise value. But for most advisors, “business planning” means recommending life insurance policies and buy sell agreements with business owners.

“Estate planning” usually means retitling assets and establishing an irrevocable life insurance trust that is funded with a whole life second to die insurance policy.

“Balance sheet analysis” is encouraging the client to take a mortgage on a vacation home, rather than pay cash, so that the advisor can keep managing assets.

Real financial planners are usually experts in one of these areas, and pseudo experts in many others. They provide deep analysis to save the clients’ money now or later and encourage the client to apply the savings against stated financial goals.

Effort

Effort is committing to be up to date on the client’s entire situation so that any change is swiftly implemented. It’s about being proactive and diligent.

And this means ALL of their financial situation, not just their investment account. Also, this is more than simply an “annual review” with the client to make sure everything is on track and the client doesn’t want to fire them.

While many clients don’t need to see their advisor quarterly, the advisor needs to have an open door to talk about any issue regarding money—at any time.

Advisors should know when clients refinance their home, switch jobs, receive a promotion, lose a loved one, or send their kids to college. Any of these instances are fair game for a phone call and meeting to discuss potential changes.

Waiting years to hear from a client, and missing all the planning opportunities in the meantime, is simply not doing your job as the trusted advisor.

Accountability

Advisors provide accountability for client saving and spending goals and encourage firm commitment to an investment strategy.

Here’s an example:

Client works at a massive tech company and is eagerly awaiting the first vest date of his shares. Advisor and client spend a few hours together well ahead of the vest to determine how to allocate the share proceeds against financial priorities. They determine that 20% will go to 529 plans for children, 40% will go towards paying off a very ugly student loan, and 40% will go to long term savings.

This one event takes them “out of the hole”, which is a HUGE step for younger folks.

One week ahead of vest the client calls and says “So my wife and I were up in Vermont and we fell in love with the area. We’re thinking of using the money as a down payment on a condo.”

The advisor immediately calls a meeting to explain to the client why this does not make financial sense and will potentially delay or derail many of their stated long-term goals.

This happens ALL THE TIME.

The client’s behavior contradicts their goals and desires.

This is just like the person that “really wants to lose weight” but eats fast food twice per week.

Advisors hold you accountable for your actions. Sure, we can’t MAKE you follow the plan, or keep you from buying a condo in Vermont to the detriment of your financial health, but we can force you to understand the consequences of your decision. We can show that it doesn’t make any financial sense.

After years of this, it’s easy to see why you would be in a better financial position.

Findings ways to save, encouraging savings to be invested and keeping clients from abandoning a strategy for the WRONG reasons is the true value add of an advisor.

Disclosure: Claro Advisors LLC ("Claro") is a registered investment advisor. Advisory services are only offered to clients or prospective clients where Claro and it's representatives are properly licensed or exempt from licensure.

Past performance shown is not indicative of future results, which could differ substantially.

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor's particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor.

The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward‐looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.