EMoney

EMoney Fidelity

Fidelity Schwab

Schwab

Tax Deferral on Capital Gains: The Qualified Opportunity Zone Investment

Invest Money Now, Pay Taxes Later

After the largest tax overhaul in thirty years, lawyers and accountants worldwide are burning the midnight oil to sift through all the new laws to best position their clients for tax efficiency.

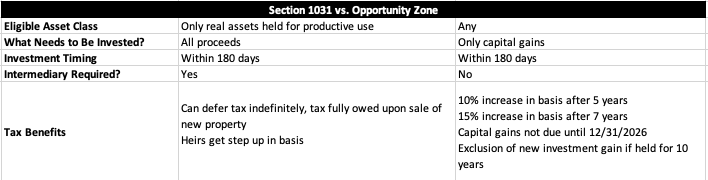

A little discussed provision of the Tax Cuts and Jobs Act of 2017 allows for investors to invest taxable capital gains directly into a Qualified Opportunity Fund ("QOF") and defer paying taxes. There is a 10% and 15% basis increase after holding the QOF for five and seven years, respectively. Any gains on QOF investments are tax free if there is a holding period of ten years or longer.

This is being compared to the very popular 1031 exchange, where real estate investors can defer gains on the sale of their property by reinvesting the entire proceeds into another investment property. 1031 exchanges are attractive to real estate investors because they can (1) reinvest their gains and taxes through deferral and (2) hold new properties indefinitely to, in effect, create a permanent gain exclusion for their heirs.

I understand that all sounds like tax speak, but basically the 1031 exchange is massive break enjoyed by generations of wealthy real estate investors.

Here's a comparison of 1031 vs. QOF.

One key difference to note is that the only the gain should go into the QOF investment, which allows sellers to free up the portion of their proceeds that represents their basis. So if someone sells an asset for $400,000 with a $200,000 basis (a gain of $200,000), they can put only the gain into the QOF, while having freed up their basis proceeds for any sort of reinvestment. This is a stark difference form the 1031 exchange, which mandates that all proceeds go into the receiving investment.

The QOF now allows this type of exchange for nearly all capital gain property, including real estate, business assets, stocks, bonds or collectibles. There is an estimated $5 trillion in taxable stock gains floating in the US--all of which could qualify for QOF investments.

Again, the basic advantage of a QOF investment held for 10 years is:

- Defer taxes on gains for any capital asset until 12/31/2026 by placing gain in QOF

- If the QOF is held for five years, the original capital gain is reduced by 10% (through a stepped up basis)

- If the QOF is held for seven years, the original capital is reduced by 15% (through a stepped up basis)

- If the QOF is held for ten years, all the QOF capital gain is excluded

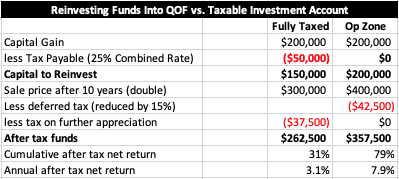

Again, let's assume that someone has a $200,000 taxable gain on the sale of a business. We will compare how a QOF investment can substantially improve post-tax returns over the traditional strategy of (1) paying taxes in year of sale and (2) placing remaining proceeds into a stock account. To do that, we'll just assume that the QOF and stock account have the same rate of return (they double over a ten year period). Here are the numbers:

Using the opportunity zone strategy more than doubles the after tax return over a ten-year period. As the old saying goes "It's not what you make, it's what you keep." In this example, our folks both "make" the same from an RoR standpoint, but the QOF strategy doubles the take-home pay.

Who Should Use This Strategy?

In my opinion, there are four key areas where this might be attractive:

- Business Owners With Liquidity Events: Tax consequences have always played a major role in structuring the sale of a business. 1031 exchanges and installment sales were the key strategies, but QOFs could be another option. Business owners could have flexibility and liquidity with the portion of the proceeds that represent return of basis, and structure QOF investments as a longer term growth strategy.

- Folks Nearing Retirement: After years of a bull market, folks that are less than five years from retirement should seriously consider shifting their portfolio out of equities and into less correlated assets. Rebalancing often brings tax consequences, and by using a QOF, a portion of the proceeds from equity sales could go into longer-term real estate holdings. Again, the equity return of basis would be still be available for immediate investment in less volatile liquid securities.

- Real Estate Investors: While the 1031 exchange is available, there isn't always a good real estate investment for tax deferral. Also, basis is tied up indefinitely. With the QOF strategy, real estate investors can liquidate part of their holdings, and gain diversification through a QOF fund.

And of course, the main drive of all these strategies is the tax benefits.

Risks/Concerns: We don't want the tax benefits-tail to wag the dog. It is absolutely imperative that anyone considering this strategy talk to their tax advisor, attorney and investment advisor to make sure that it fits into their overall plan and strategy for personal financial goals. Here are the major downsides.

- Illiquidity: The QOF investment is likely a ten-year hold. If the time-horizon for funds is shorter than ten years, in almost any scenario, the QOF may not be appropriate.

- Lack of Current Income: QOF are development projects so it's unlikely that they will provide any sort of operational income for the first few years. While income is possible, investors should look elsewhere for stable income and view QOFs as long term growth plays.

- Lack of Deals: QOF managers are aggressively seeking properties that qualify for this tax treatment. There is an expected influx of cash into QOFs due to the tax benefits, and with only so many approved tracts, deals could be bid well above fundamentally sound prices.

- Uncertainty of Legislation: This is the first pass at the legislation. While managers and tax advisors are doing their best, there are still many questions around this. It is not outside the realm of possibility that a perceived QOF makes a mistake and runs afoul of tax laws. That could undermine the entire strategy.

- High Fees: Most funds are run like a private equity fund with very high fees--both management fees and carried interest (along with all the other traditional real estate fees). Although the expected returns net of fees still look attractive, high fees can undermine returns. Choose a fund with a low management fee and a high hurdle.

For folks with large gains and the need to diversify into an income producing investment, the opportunity zone fund strategy may be appropriate.

Disclosure: Claro Advisors, LLC ("Claro") is a registered investment advisor with the U.S. Securities and Exchange Commission ("SEC"). The information contained in this post is for educational purposes only and is not to be considered investment advice. Claro provides individualized advice only after obtaining all necessary background information from a client. Please contact us here with any questions.