EMoney

EMoney Fidelity

Fidelity Schwab

Schwab

How Can Confidence Kill Investment Returns?

"Too much information can serve to artificially inflate our confidence so that we increase our bets without any greater ability to predict the outcome of future events."

Adam Robinson is a macro global advisor to some of the largest hedge funds and ultra-high-net-worth family offices. As a child, he was a chess prodigy tutored by the legendary Bobby Fisher. As a young adult, he created the now ubiquitous Princeton Review SAT prep course—which he later sold for a handsome reward. Based on my admittedly limited knowledge of Robinson, his “magic” lies in developing mental models for key decisions to maximize performance and efficiency. He’s like a chess master for life.

In a recent interview, the interviewers asked Adam what types of “bad advice” he often hears related to his profession of global finance and investing. Adam responded with an interesting story that has profound value for all types of investors.

The core of the lesson is that, despite what we often hear in boardrooms and classrooms across the globe, more information does not necessarily translate to better results. On the contrary, too much information can serve to artificially inflate our confidence so that we increase our bets without any greater ability to predict the outcome of future events. In other words, additional information can cause us to “double down” on our own biased and flawed opinions—which results in poor investment returns.

The Paul Slovic Horse Racing Study

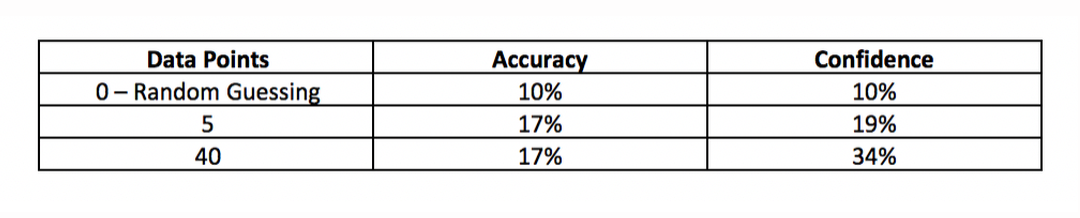

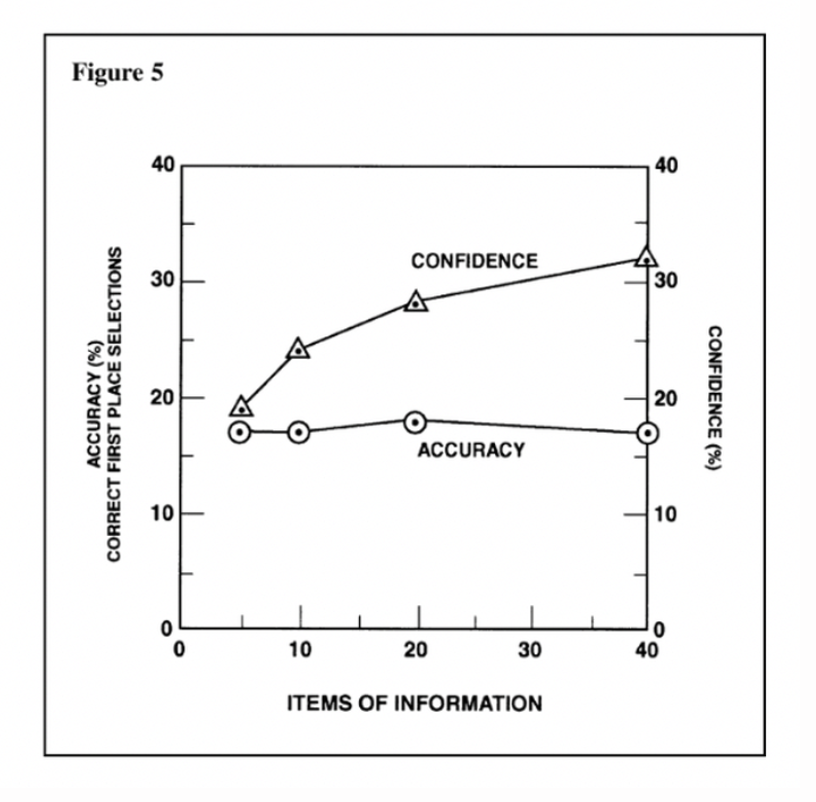

Robinson cites a study from 1973 where Paul Slovic studied several professional horse handicappers—individuals that made their living on horse betting. The handicappers were given various amounts of information for purposes of making their bets. The researchers tracked the success and confidence of each handicapper as more information became available. Keep in mind, the study group were such good handicappers that they made a living from it—these weren’t just casual trackers.

The study went as follows. First, the handicappers had to predict the outcome of a set of races with no information about race participants. For the next race, the handicappers were given five requested pieces of information. Then ten pieces. Then twenty pieces. And finally, FORTY pieces of information for the last set of races.

With each race, the researchers tracked (1) accuracy of prediction and (2) confidence.

Here are the results:

While a small amount of information increased the accuracy of predictions by about 70% (10% to 17%), the information above five percent only served to increase confidence. Accuracy flatlines at 17%, but confidence shoots to 34% when forty pieces of information became available. With higher confidence, the handicappers increased their bets without any higher accuracy—and this ultimately produced worse overall results. Here is a description of the unpublished study from the official website of the US Central Intelligence Agency in a titled “The Psychology of Intelligence Analysis.”

The lesson is that beyond some small amount of useful information, we use additional information to feed our existing biases. Contrary information is ignored or dismissed, where additional complementary information feeds and reinforces our flawed view.

This practice is called confirmation bias, and here’s how it happens.

- Based on certain evidence, we hold opinion X and DO NOT hold contrary opinion Y.

- As more facts become available, we incorporate those that support our case for opinion X, but ignore any facts that that support contrary opinion Y.

- We are now very confident in opinion X, despite there being as much or more objective support for opinion Y (which we have ignored).

Figure 1: Source - https://www.cia.gov/library/center-for-the-study-of-intelligence/csi-publications/books-and-monographs/psychology-of-intelligence-analysis/fig5.gif/image.gif

{kind=link}

Additional support is feeding confidence, and then we become destructive. As Mark Twain said,

“It ain’t what you don’t know that gets you into trouble. It’s what you know that just ain’t so.”

Robinson then ties this study to global investing (emphasis added).

…we think we understand the world, giving investors a false sense of confidence, when in fact we always more or less misunderstand it.

You hear it all the time from even the most seasoned investors and financial “experts” that this trend or that “doesn’t make sense.” “It doesn’t make sense that the dollar keeps going lower” or “it makes no sense that stocks keep going higher.” But what’s really going on when investors say that something makes no sense is that they have a dozen or whatever reasons why the trend should be moving in the opposite direction... yet it keeps moving in the current direction. So they believe the trend makes no sense. But what makes no sense is their model of the world. That’s what doesn’t make sense. The world always makes sense.

In fact, because financial trends involve human behavior and human beliefs on a global scale, the most powerful trends won’t make sense until it becomes too late to profit from them. By the time investors formulate an understanding that gives them the confidence to invest, the investment opportunity has already passed.

So when I hear sophisticated investors or financial commentators say, for example, that it makes no sense how energy stocks keep going lower, I know that energy stocks have a lot lower to go. Because all those investors are on the wrong side of the trade, in denial, probably doubling down on their original decision to buy energy stocks. Eventually, they will throw in the towel and have to sell those energy stocks, driving prices lower still.

Where does confirmation bias eat away at our returns, financial or otherwise? Next time you’re sure of something, remember this study and think about all the information that you choose to ignore.

For more information on this and other investment advice contact Bob Dockendorff or subscribe to his monthly email newsletter "Goals Mining".

Disclosure: Claro Advisors, LLC ("Claro") is a registered investment advisor with the U.S. Securities and Exchange Commission ("SEC"). Information contained herein is for educational purposes only and is not to be considered investment advice. Claro provides individualized advice only after obtaining all necessary background information from a client. Information contained herein is taken from sources believed to be reliable, but cannot be guaranteed as to its accuracy. It is for informational and planning purposes. Nothing herein shall be construed as an offer or solicitation to buy or sell any securities. Nor is it legal or accounting advice. Investing carries risks and expenses and involves the potential loss of investment. Past results are not indicative of future results.