EMoney

EMoney Fidelity

Fidelity Schwab

Schwab

A Measured Approach to Evaluating Long-Term Care Needs

Long term care is a grim but necessary topic for older Americans. It’s easy to understand why most folks would ignore this issue.

Long-term care is unpleasant, expensive and there are few palatable ways to fund the expense. Unfortunately, the issue isn’t going away, and the earlier folks consider the problem, the sooner they’ll find a viable solution.

For purposes of retirement planning, the most productive way to think about long-term care (and funding options) is to consider the need for long-term care to be more likely than not contingent event and to view any insurance policy as the pre-funding of a future expense (for more on this read the always fantastic Michael Kitces).

Unlike other insurance that requires a small premium to cover a catastrophic but unlikely contingency, long-term care is statistically probable for most people.

But recognizing the need and planning for the expense are two very different things. The obvious and unanswerable questions include:

Why type of care will I need?

When and how long will I need it?

How much will it cost?

We can’t answer these questions today, but we can develop assumptions based on available information and use those in our retirement plans.

One good place to start, for everyone, is the macro data on long-term care needs and cost:

Based on the numbers, people should assume they will need about three years of long-term care in their 80s.

That is a total long-term care need of about $300k per person, in today’s dollars. For a 65-year old we can assume 15 years of growth, and the number becomes $442k of needed long-term care coverage, adjusted for inflation.

Also, note that folks should adjust these numbers for their geographic location. The current annual cost of a nursing home private room in Ohio is $96k but is significantly higher in states like Massachusetts where the cost is $150k. Make sure you’re insuring for the state where you’ll receive care.

Ok, here’s the first question every 65-year-old should answer: What happens to your retirement expense if we add an additional $442k expense over three years in your early eighties?

For those that can’t fathom such an expense (most people), you should consider Medicaid planning.

For those with more than modest assets, do the following to determine your “cost of care” number:

-

Determine the annual cost of a private nursing home in your state

-

Multiply it by three for the average number of years individuals need care

-

Subtract your current age from 80

-

Grow (2) by a compounding 3% compounding for the number of years until age 80

If you’re 55 and live in Massachusetts, the calculation would be as follows.

-

The average annual cost of a private room in a nursing home is $150k

-

$150k x 3 = $450k

-

80 – 55 = 25 years

-

$450k*(1+2%)^25 = $738,273

Now take your “cost of care” number and run a retirement projection to see how it affects your chances of retirement success. If a long-term care event brings your chances of success to a level you’re not comfortable with, say 65%, then do the following.

-

Obtain a quote for sufficient long-term care insurance

-

Add the premium to your retirement expense plan

-

Run the plan with insurance, and then both with and without a long-term care event

If you can’t pay for enough coverage without derailing your retirement plan, then consider Medicaid planning. But for those that can afford the premium and significantly reduce the impact of a long-term care event, strongly consider purchasing private long-term care insurance.

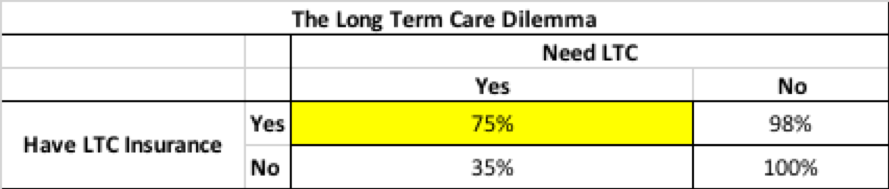

Here’s an example for our 55-year-olds above. The percentages refer to the chance that our retiree has of making not outliving their money based on a 1,000 random investment return scenarios.

You can see that under the base plan (No LTC, No Insurance) they have 100% chance of success. With LTC need, but no coverage, they only survive 35% of the time. These are the extremes. But if we (1) add in the cost of long-term care they have at least a 75% chance of not outliving their money. And if they buy the premiums but never need the insurance, they still have a 98% chance.

In this instance, I would heavily recommend purchasing the coverage. We haven’t solved the problem of growing premiums or forfeiture of premiums.

For the Millionaires

What about the folks that can afford long-term costs? This includes retirees with several million dollars that can absorb long-term care costs without risking their chances of a successful retirement.

In this case, it becomes more about optimizing to save on potential long-term care costs through asset repositioning and the use of a hybrid insurance policy.

Imagine you’re 55 years old and plan to have $3mm when you retire at age 67—more than enough to sustain living and potential long-term care expenses. One third, about $1mm, of your portfolio will have exposure to low-volatility cash and fixed income investments.

What if you could take $100k of those assets (3.3% of all assets) and “park” them into a whole life insurance policy that offers a death benefit, cash value and $250k of long-term care benefit growing at a compounding 3%. You can also start “parking” that $100k over ten years prior to retirement at an equal $10k per year.

From a linear cash flow stand-point, this strategy would help absorb the cost of long-term care without risking the principal and keeping foregone investment returns at a minimum as those funds were earmarked for low return asset anyways.

Looking at the projected costs of long-term care, foregone investment growth and hybrid premiums, the following chart shows the ultimate cost of all scenarios.

Using the same chart above we can see the cost of each scenario. I kept it in today’s dollars, which doesn’t account for growth or inflation. The cost of having, and not needing a hybrid insurance policy is low because there is a cash value and repayment of premium. For those with significant assets, this cost is negligible.

The benefit, however, is significant as the cost savings in the (more likely than not) long-term care event is $194k, ($364k - $170k).

The asset repositioning strategy is attractive for high net worth individuals.

Conclusion

Without having any perfect way to plan for long-term care, this framework provides at least a reference point to conduct analysis for purchasing LTC insurance. Each individual should speak with their financial planner and insurance professional to tweak assumptions for any specific available facts. Overall, with statistics and best/worst case scenarios, we seek to achieve the highest likelihood for a comfortable, stable, and predictable retirement.

If you need help, schedule a call with Claro Advisors here.

Disclosure: Claro Advisors, LLC ("Claro") is a registered investment advisor with the U.S. Securities and Exchange Commission ("SEC"). Information contained herein is for educational purposes only and is not to be considered investment advice. Claro provides individualized advice only after obtaining all necessary background information from a client. Information contained herein is taken from sources believed to be reliable, but cannot be guaranteed as to its accuracy. It is for informational and planning purposes. Nothing herein shall be construed as an offer or solicitation to buy or sell any securities. Nor is it legal or accounting advice. Investing carries risks and expenses and involves the potential loss of investment. Past results are not indicative of future results.