EMoney

EMoney Fidelity

Fidelity Schwab

Schwab

How High Earners Can Fund Roth Accounts - A Few Strategies

High Earners, You Can Fund Roths Too

Two Ways HighEarners Should Fund Roth Accounts

Roth accounts are the holy grail of retirement savings. While taxed in the year of contribution, once in a Roth, funds are tax free forever. No tax on investment, or withdrawals, or even distributions to your kids when you’re gone and they’re fighting over your estate.

But high earners face an uphill battle in funding Roth accounts. Direct contributions to a Roth IRA aren’t allowed for households earning more than $203,000. So that’s out.

Also, contributing to your Roth 401(k) probably isn’t worth it

Many employer plans allow for Roth contributions instead of, or in conjunction with, traditional pre-tax contributions. The maximum annual contribution is $19,000 in 2019, with an additional $6,000 “catch up” contribution for employees over fifty.

This technically allows high-earning employees to make a meaningful Roth contribution, but at the cost of making valuable pre-tax contributions. For instance, an employee at a combined federal and state tax rate of 43% receives a tax savings of roughly $11,180 on a $26,000 traditional 401(k) contribution. We assume the employee’s withdrawal rate will be lower later. It’s better to take the tax savings now. I almost always encourage traditional contributions for high earners.

So, how’s a high earner supposed to use a Roth?

There are two key strategies:

-

The Back-Door Roth: A low and slow, long-term strategy that works.

-

The Super Roth: A high-impact strategy for super savers.

The Back-Door Roth Conversion

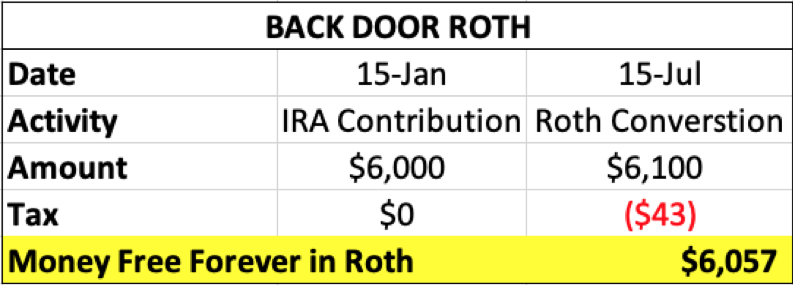

This is a very popular strategy in which folks can contribute $6,000 per year ($7,000 if over 50) through a series of transactions.

First, there is a nontaxable contribution to an IRA for the maximum amount, which we’ll suppose is $6,000 here. The funds sit in the IRA for about six months (sometimes they’re invested). Six months later (same twelve-month period), there is a Roth conversion for all funds.

Why This Strategy Works

Unlike other Roth conversions, there is minimal tax impact because the original IRA contribution was post-tax. For that reason, there is no tax paid on conversion of the $6,000 (the “basis”), but tax may be owed on any investment growth. If we assume there was $100 in investment growth and a 43% tax rate, here’s how it would work:

After years and years..and years and years and years of doing this, it makes a meaningful difference in someone’s financial profile. Think about starting this at age 30 or 35 and doing it until age 67.

At retirement there is a massive Roth balance, and it cost almost nothing from a tax standpoint.

Financial planning win.

Option 2 - The Super Roth: The Better Option for Post-Tax Savings

Despite the exciting name, this unfortunately still has to do with Roth accounts, but…

The Super Roth is becoming more popular in employer plans. It allows for post-tax savings AFTER the maximum contribution to a 401(k).

Here’s an example:

If you’ve ever said, “Well, I’ve maxed out every available retirement plan for this year, but still have a bunch of money lying around—what should I do with it?”

I would say… “This strategy is for you. And also, you’re kind of annoying.”

Just kidding.

“But didn’t you say that that I have too high of a tax rate for Roth?”

Yes, but this is a different analysis. This is no longer Roth vs. Pre-tax, as traditional contributions are not available for this money. It’s now Roth vs. other investment vs. spending.

Most of the time the other investment is just a brokerage account—so why not use a brokerage account that can’t create tax liabilities?

Barring some exceptional investment opportunity or lifelong desired purchase, I would say put a bunch of that money into the Super Roth and still have plenty of funds leftover for golf memberships and avocado toast.

The max Super Roth amount will depend on your employer plan. It can go as high as $37,000.

Note: It’s not technically a “Roth” account, but the IRS issued guidance that these post-tax retirement funds can be directly rolled over into a Roth IRA—so in substance, it’s a Roth.

If you’re earning too much money to directly contribute to a Roth, use one of these strategies to improve your tax profile in retirement.

Disclosure: Claro Advisors LLC ("Claro") is a registered investment advisor. Advisory services are only offered to clients or prospective clients where Claro and it's representatives are properly licensed or exempt from licensure.

Past performance shown is not indicative of future results, which could differ substantially.

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor's particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor.

The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward‐looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

Index returns are unmanaged and do not reflect the deduction of any fees or expenses. Index returns reflect all items of income, gain and loss and the reinvestment of dividends and other income. You cannot invest directly in an Index.